This is an internship project aiming to make Attribution Analysis for general equity funds in China market

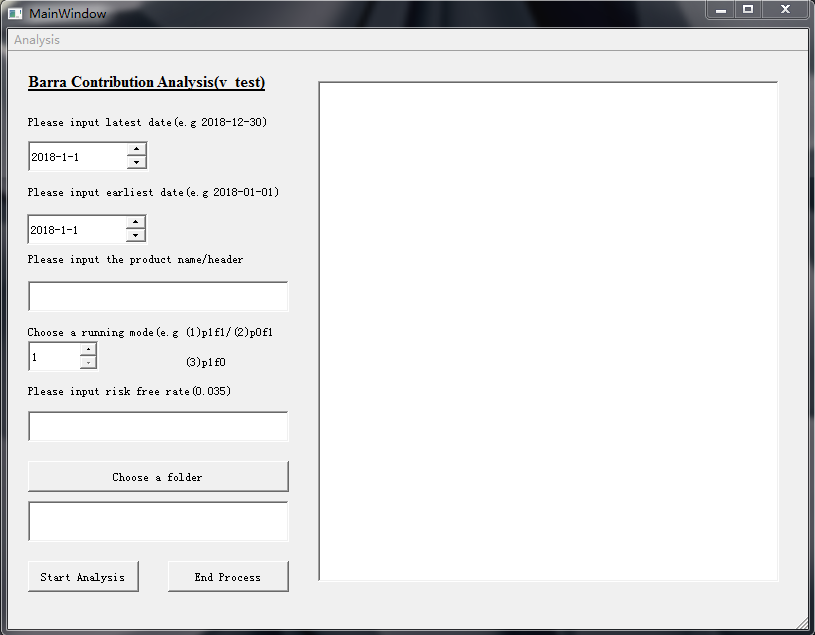

The whole process of making Factor Attribution is complicated and demanding. All works done here are assuming users have already had daily factor exposures and daily factor returns per unit and all other necessary data prepared. Basically, I only did some jobs on calculation part instead of making things on scratch. To be clear, this project has three modes: p1f1(portfolio with both stocks and futures)/ p1f0(pure stocks portfolio)/p0f1(pure futures portfolio).

This project consists of three parts. Respectively, they are index calculation, Factor Attribution and program building.

This part is only meant for those who don' t have index weight data

This is the main body of this project, also mostly used during my internship.

This part is currently under experiment stage, and partialy for fun.